It is the last Friday of the month, and the start of a holiday weekend, so time to clear off the desktop of items I have been meaning to get to.

Soda

I will kick it off with a story from Salt Lake City. It seems that a public high school in suburban (exurban?) Kaysville, Utah has been fined $15K by the Feds.

As we all know, it is a Federal offense to sell carbonated beverages at public school lunches. Davis High had arranged to turn off their vending machines during the 47 minutes allotted daily for lunch, but they overlooked the fact that their bookstore also sold the vile liquid. Luckily, Federal inspectors caught it and stopped the madness.

Read more »

Normally, this is the time of year that money advisors and gurus trot out the old canned advice on end-of-year tax planning. Not this year. This year we are all just too confused.

Generally, we can do little things in November and December to slightly lower our tax bill because, generally, we can predict what the tax rates will be in January. Not this time. Congress managed to adjourn for the elections without doing anything at all about the expiring Bush tax cuts, and when they  reconvene for the lamest of lame duck sessions today I do not foresee a sudden clarity of purpose.

reconvene for the lamest of lame duck sessions today I do not foresee a sudden clarity of purpose.

Could there have been any larger indication that the Democrats were in very serious trouble than that they passed up an opportunity to enact tax cuts a few weeks before an election? Yes, there were (and are) differences of opinion on what bits of the Bush cuts should be extended, but those differences ought to have been bridgeable. Instead, the Democrats became frozen in fear and indecision, petrified (and not entirely without reason) that any legislation they passed, whatever the particulars, would cost votes.

Read more »

As a cap to Complain About Taxes Week, I thought it would be amusing to peruse somebody else’s tax return. There are not very many publicly available ones to choose from, but there is this one from a famous multi-millionaire author.

11 Slightly Interesting Things From the Obamas’ 2009 Tax Return

1. The social security numbers are redacted. The White House provided most of the 1040 and schedules that were filed, but the SSN boxes are blank. I guess there is the potential for political pranks, but seriously, what are the chances of somebody trying to use Barak Obama’s identity to open a new credit card?

1. The social security numbers are redacted. The White House provided most of the 1040 and schedules that were filed, but the SSN boxes are blank. I guess there is the potential for political pranks, but seriously, what are the chances of somebody trying to use Barak Obama’s identity to open a new credit card?

2. Both Obamas sent $3 to the presidential election campaign fund. A classy thing to do given that Obama is the only major party candidate in history to turn down money from the fund. Presumably, he won’t use it in 2012 either, so this just helps the other guy.

Read more »

As April 15 approaches, some of us experience a short-lived obsession with, and resentment of, taxes. For fairly obvious reasons, those of us who put off  sending in the old 1040 until the last minute tend to be those who need to accompany our returns with checks made out to the Treasury. Folks entitled to checks going the other way tended to file weeks ago.

sending in the old 1040 until the last minute tend to be those who need to accompany our returns with checks made out to the Treasury. Folks entitled to checks going the other way tended to file weeks ago.

Having to fill out lengthy government forms is bad enough. Capping off the process with a savingsectomy is enough to turn anybody into a grumpy Republican. For me, this is like being an Irishman on St. Patrick’s Day. I enjoy the company of my temporary compatriots, even though I know it won’t last long.

Pandering to this grumbling constituency this week was The Big Money, which shared a list of the five worst parts of the tax code. The fact that they could come up with only five tells me they are only seasonally grumpy. A year-round resident would have come up with at least ten.

Read more »

I have been giving a lot of thought to the federal budget deficit lately. Well, some thought. Not as much thought as I have been giving FiLife’s March Money Madness 16 blog tournament. I’m pretty sure they had 15 likely blogs and threw in BMA just to round out the field and add some humor.

Alas, I digress. As all us good Republicans know, the first step in closing the budget gap should be a massive reduction in government spending. I’d start with the TSA and agriculture subsidies, but that’s just me.

start with the TSA and agriculture subsidies, but that’s just me.

And we’ve got to cut out these loss-making wars. Next time we invade an oil-rich country we need to actually take the oil. Everybody else will accuse us of going to war to get the stuff anyway, so we might as well cash in.

More digression. Sorry.

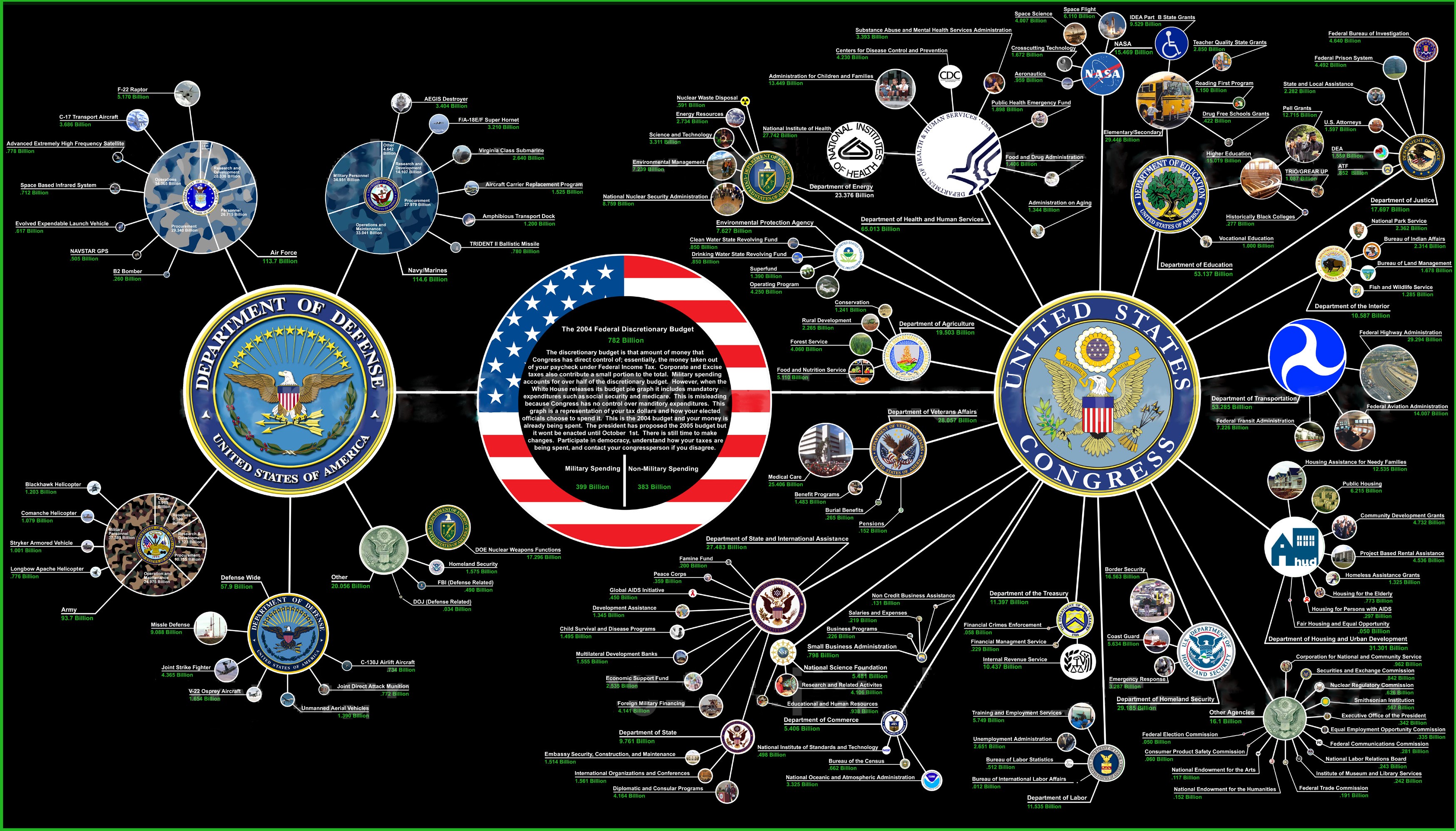

A quick glance at the federal spending pie chart will tell you that the bits of the budget that can be cut in the short run are not big enough to eliminate the deficit. (For a further, but somewhat out of date, breakdown that could turn anybody into a libertarian, if not an anarchist, click here.) It breaks my heart to say it, but we need some new taxes. Here are my suggestions.

Read more »

{kind=link}